This article presents export and import functions based on the imperfect substitutes model summarized by Goldstein and Khan (1985).

Key words: export, import, exchange rates, demand, supply, economic models

В статье изучается использование функции экспорта и импорта в эмпирических целях, основанные на модели несовершенных заменителей, обобщенной Гольдштейном и Ханом (1985).

Ключевые слова: экспорт, импорт, обменные курсы, спрос, предложение, экономические модели

The empirical specification of export and demand functions in this paper basically relies upon the imperfect substitutes model summarized by Goldstein and Khan (1985). We used this approach because the model is simple and also summarizes all the main determinants of trade flows between nations. The imports of a country are a function of import prices, exchange rates and the country’s income and general price level while theexports are a function of export prices, exchange rates as well as incomes and price levels of the country’s trading partners. The central assumption of the model is that the traded products between importer country and exporter country are not completely homogenous; e.g. they do not render a perfect substitutability between each other in consumption. This assumption is quite realistic and has found extensive empirical support. Ostry and Reinhart (1992) conducted a study in which the intra-temporal elasticity of substitution between traded and non-traded goods was estimated for a broad number of developing countries. The estimated parameter lied between 1.0–1.5 in all the regions under study implying their gross substitutability[1]. Imperfect substitutability also found its empirical confirmation in later works of Ogaki, Ostry and Reinhart (1994). Besides, it is also assumed that, both import and export products are consumed by the representative agents together with domestic products. Agents derive their utility in each period by Cobb-Douglas utility function. The utility optimization subject to the agents’ flow budget constraints yields representations of both import and export demand equations which can be specified as Marshallian demand functions.

Empirical literature on trade flow relationship has a long and vast history. From the outset of empirical investigation the works on international trade flows were concentrated more on the significance and consistency of price and elasticity coefficients using OLS methods. However, that the estimation results could be biased due to endogeneity problems caused by the simultaneity of the import and export quantities together with their prices was pointed out in 1950s (Orcutt (1950), Harberger (1953)). Endogeneity problems were addressed following decades by authors such as Goldstein and Khan (1978) and Marquez and McNeilly (1988). Their proposition was to use simultaneous equation models to avoid endogeneity biases. Furthermore, in their later works, these and other authors also made proposals of the use autoregregressive distrubutive lag models to account for autocorrelations and moving average features in the times series under consideration that might bias OLS estimations.

Later works more focused on testing and incorporating the inherent non-stationarity feature into the time series model. In 1990s, the studies of Rose (1991), Senhadji and Montenegro (1998, 1999), and Reinhart (1995) have shown that the imports, exports and their relative prices are all unit root processes. The presence of unit roots may seriously bias OLS estimator despite its BLUE characteristics and lead to spurious regression. This has made the identification of the features of time series data an important element in the analysis. In such a scenario (which we recognize with our data), the empirical literature recommends the use of estimators such as the Dynamic OLS (Phillips and Hansen (1990), Phillips and Loretan (1991), Saikkonen (1991)) or the Fully Modified Least Squares (FMLS) (Phillips and Hansen (1990), Hansen (1992). For the multivariate case, the Johansen’s (1988, 1997) cointegration approach is used.

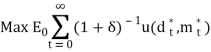

This paper employs the a methodology of Senhadhi and Montenegro (1999), a slightly different approach but yet based on imperfect substitutes model. Assume the number of trading partners of the exporting country (home country) is limited only to one country (foreign country). Then exporter’s demand function will be the same as the importer’s demand function. This idea has been developed further for the import model developed under this paper. Another assumption involved is that the import decisions are made by an infinitely long lived agent who decides how much to consume from his domestic good (![]() ) and of the imported good (

) and of the imported good (![]() )[2], which is identical to the export demand of the home country (

)[2], which is identical to the export demand of the home country (![]() ). The intertemporal decision of the representative agent from the foreign country is formalized by the following optimization problem:

). The intertemporal decision of the representative agent from the foreign country is formalized by the following optimization problem:

|

|

(1) |

|

subject to: |

|

|

|

(2) |

|

|

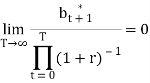

(3) |

|

|

(4) |

where:

![]() is the world interest rate;

is the world interest rate;

![]() is the next period stock of home bond held by the foreign country if positive and the next period stock of foreign bonds held by the home country if negaitve

is the next period stock of home bond held by the foreign country if positive and the next period stock of foreign bonds held by the home country if negaitve

![]() is the stochastic endowment which follows an AR(1) process with unconditional mean

is the stochastic endowment which follows an AR(1) process with unconditional mean ![]() and unconditional variance

and unconditional variance ![]() where

where ![]() is the variance of iid innovation

is the variance of iid innovation ![]() and

and ![]() determines the degree of persistence of the endowment stock;

determines the degree of persistence of the endowment stock;

![]() is the price of the home good in terms of foreign good.

is the price of the home good in terms of foreign good.

Equations (2)~(4) are respectively the current account equation, the stochastic process driving the endowment shocks, and the transversality condition rules out Ponzi-schemes. The first order conditions of this problem are:

|

|

(5) |

|

|

(6) |

|

|

(7) |

where:

![]() is the Lagrange multiplier on the current account equation (2). From equation (5),

is the Lagrange multiplier on the current account equation (2). From equation (5), ![]() is the foreign consumer’s marginal utility for domestic good. Following Ogaki (1992) and Clarida (1994),

is the foreign consumer’s marginal utility for domestic good. Following Ogaki (1992) and Clarida (1994), ![]() is assumed to be a addilog instantaneous utility function:

is assumed to be a addilog instantaneous utility function:

|

|

(8) |

|

|

(9) |

|

|

(10) |

where

![]() and

and ![]() are exponential stationary random shocks to preferences;

are exponential stationary random shocks to preferences;

![]() and

and ![]() are stationary shocks;

are stationary shocks;

Substituting equation (8) into equations (5) and (6) yields:

|

|

(11) |

|

|

(12) |

Substituting equations (9)~(11) into equation (12) and taking logs of both sides yields:

|

|

(13) |

where:![]() and

and ![]()

Senhadhi and Montenegro (1999) created an activity variable here replacing ![]() . However, we will not deviate from standard model and use

. However, we will not deviate from standard model and use ![]() for

for ![]() . Then equation (13) can be rewritten as

. Then equation (13) can be rewritten as

|

|

(14) |

This is the basic equation to go further when estimating exports and imports.

This article showed how to derive export and import function based on conventional economic models. The article also showed that solving optimization problem for representative agent’s decision on import consumption can be used to develop empirical equation of the import function.

Further research is needed to estimate expert/import function parameters using data on export and import flows. Such exercise will also helpful to conduct robustness tests of the derived export/import functions.

References:

- Bardhan, P. L. (1970). Models of Growth with Imported Inputs. Economic, 37 (148), 373–385.

- Clarida, R. (1994). Cointegration, Aggregate Consumption, and the Demand for Imports: a Structural Econometric Investigation. American Economic Review, Vol.84, 298–308.

- Goldstein, M., & Khan, M. (1985). Income and Price Effects in Foreign Trade. In R. Jones, & P. Kenen, Handbook of International Economics, Vol.II (pp. 1041–105). Amsterdam: North-Holland.

- Goldstein, M., & Khan, M. (1978). The Supply and Demand for Exports: A Simultaneous Approach. The Review of Economics and Statistics 60 (2), 275–286.

- Hansen, & Bruce. (1992). Efficient Estimation and Testing of Cointegrating Vectors in the Presence of Deterministic Trends. Journal of Econometrics, Vol. 53, 87–121.

- Harberger, A. C. (1953). A Structural Approach to the Problem of Import Demand. The American Economic Review 43 (2), 148–159.

- Khang, C. (1968). A Neoclassical Growth Model of a Resource — Poor Open Economy. International Economic Review, Vol.9, 329–338.

- Kurpayanidi, K. (2015). Innovation component of the business environment as a factor enhancing economic growth. Economics, (1), 6–9.

- Kurpayanidi K., Muminova E., Paygamov R. (2015) Management of innovative activity on industrial corporations //Monograph. LAP LAMBERT Academic Publishing. Germany.

- Kurpayanidi, K. I. (2017). improving corporate governance system as a factor of economic growth in strategic sectors of the national industry of Uzbekistan. Актуальные проблемы гуманитарных и социально-экономических наук, 5(11), 123–125..

- Makhmudova N. A. (2016) Modern taxation of private entrepreneurship in Uzbekistan //Актуальные проблемы гуманитарных и социально-экономических наук. — №. 10–4. — С. 57–59.

- Maizels, A. (1968). Exports and Economic Growth of Developing Countries. New York: Cambridge University Press, 58.

- Margianti E. S. et al. (2014) Systematical analysis of the position and further development of Uzbekistan national industry in the case of economic modernization. Monograph. Indonesia, Jakarta //Indonesia, Jakarta, Gunadarma Publisher.

- Marquez, J., & McNeilly, C. (1988). Income and Price Elasticities for Exports of Developing Countries. The Review of Economics and Statistics 70 (2), 306–314.

- Phillips, P., & Hansen, B. (1990). Statistical Inference in Instrumental Variables Regression with I(1) Processes. Review of Economic Studies, Vol. 57, 99–125.

- Phillips, P., & Loretan, M. (1991). Estimating Long-run Economic Equilibria. Review of Economic Studies, Vol. 58, 407–436.

- Reinhart, M. C. (1995). Devaluation, Relative Prices and International Trade. IMF.

- Senhadji, S. A., & Montenegro, E. (1998). Time Series Analysis of Export Demand Equations: a Cross-Country Analysis. IMF.

- Villanueva, D. (1993). Exports and Economic Development. IMF Working Paper No.93/41.

[1] For perfect complementarity, the intertemporal elasticity would lie below unity and otherwise to infinite value for perfect substitutability.

[2] The variables with asterisks denote foreign